Article content

(Bloomberg) — Asian stocks are set to climb in early trading as markets parse Federal Reserve Chair Jerome Powell’s reminder that policymakers are in no hurry to ease interest rates. Gold and oil advance.

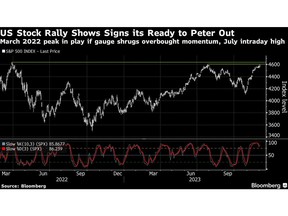

Australian shares rallied while equity futures in Japan and Hong Kong point to early gains. The S&P 500 index climbed higher Friday, to close ahead for a fifth week and reach its highest close since March 2022. Contracts in mainland China point to an early loss after the Golden Dragon Index – a gauge of US-listed Chinese shares – slumped 1% in its last session.

Article content

US stocks and bonds rallied Friday as Powell noted policy is “well into restrictive territory,” though is ready to hike further if needed. The dollar slid, two-year Treasury yields sank to their lowest since June and traders ratcheted bets on a quarter-point Fed cut in March, with swaps fully pricing in a reduction in May. They project over a full point of easing by December 2024. Australian yields fell early Monday, tracking Treasuries.

“The big rebound in shares has left them technically overbought and at risk of a consolidation or short term pull back,” Shane Oliver, head of investment strategy and chief economist at AMP Ltd. in Sydney wrote in a note to clients. “However, further gains are likely into year end and early next year as inflation continues to ease” and positive market seasonality kicks in later this month, he said.

The recent rally in US stocks and bonds comes as signs are piling up — in recent data, in warnings from top retailers and in anecdotes from local businesses across the country — that after defying expectations all year and splurging over the summer, American households are starting to pull back. A measure of US factory activity shrank for a 13th straight month in November as high interest rates continue to hammer the goods-producing side of the economy.

Article content

Oil rose while gold traded at a record level as investors kept watch on geopolitical tensions in the Middle East. Israel has resumed its military operation in Gaza, a US warship was attacked in the Red Sea and Houthi rebels in Yemen said they had carried out operations against two Israeli ships.

Elsewhere, Bitcoin hit $40,000 for the first time since May 2022, extending the year’s rebound amid bets on lower interest rates and greater demand from exchange-traded funds.

Read More: Eerie Calm in S&P 500 Signals Historic Rally Has Staying Power

Sticky Inflation

This week, traders will be monitoring for clues to the health of the global economy with Australian growth, Chinese inflation and US non-farm payrolls data all due. The Reserve Bank of Australia is expected to sound hawkish as it keeps its rate on hold on Tuesday after governor Michele Bullock warned inflation is now homegrown.

While the cooler-than-expected inflation will keep the RBA on hold, “sticky ‘homegrown’ services inflation will ensure a tightening bias is retained,” Tony Sycamore, an analyst at IG Group in Sydney wrote in a note to clients. “A rate hike in February hinges on the outcome of the December quarter inflation due for release in late January.”

Article content

In corporate news, China Evergrande Group, the world’s most indebted developer, faces a Hong Kong court hearing on Monday over a creditor request to wind up the company. US airline stocks will be in focus when Wall Street reopens Monday after Alaska Air Group Inc agreed to buy rival Hawaiian Holdings Inc.’s Hawaiian Airlines in a deal valued at $1.9 billion.

Key events this week:

- China Evergrande Group liquidation hearing in Hong Kong starts, Monday

- Riskbank November meeting minutes released, Monday

- RBA rate decision, Tuesday

- Japan’s Tokyo CPI, Tuesday

- China Caixin services PMI, Tuesday

- South Korea CPI, GDP, Tuesday

- Eurozone PMIs, Tuesday

- Australia GDP data, Wednesday

- Eurozone retail sales, Wednesday

- Bank of Canada rate decision, Wednesday

- China trade, FX reserves, Thursday

- Eurozone GDP, Thursday

- Mexico CPI, Thursday

- Germany CPI, Friday

- Japan household spending, GDP, Friday

- US non-farm payrolls, Friday

Some of the main moves in markets:

Stocks

- S&P 500 futures were little changed as of 8:27 a.m. Tokyo time

- Hang Seng futures rose 0.3%

- Australia’s S&P/ASX 200 rose 1.2%

Article content

Currencies

- The Bloomberg Dollar Spot Index fell 0.4%

- The euro rose 0.1% to $1.0895

- The Japanese yen rose 0.4% to 146.29 per dollar

- The offshore yuan was little changed at 7.1268 per dollar

- The Australian dollar rose 0.2% to $0.6689

Cryptocurrencies

- Bitcoin rose 0.4% to $39,873.63

- Ether rose 0.1% to $2,186.3

Bonds

- Australia’s 10-year yield declined eight basis points to 4.41%

Commodities

- West Texas Intermediate crude rose 1.2% to $74.95 a barrel

- Spot gold rose 1.2% to $2,098.01 an ounce

This story was produced with the assistance of Bloomberg Automation.

—With assistance from Michael G. Wilson.

Share this article in your social network