Bond Investors Are at a Crossroads With Fed Pause In Sight

Share This

The emerging consensus that the Federal Reserve will raise rates only one or two more times has ushered in a new set of dilemmas for bond investors, who now must decide which parts of the market will fare best under the circumstances.

(Bloomberg) — The emerging consensus that the Federal Reserve will raise rates only one or two more times has ushered in a new set of dilemmas for bond investors, who now must decide which parts of the market will fare best under the circumstances.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

Article content

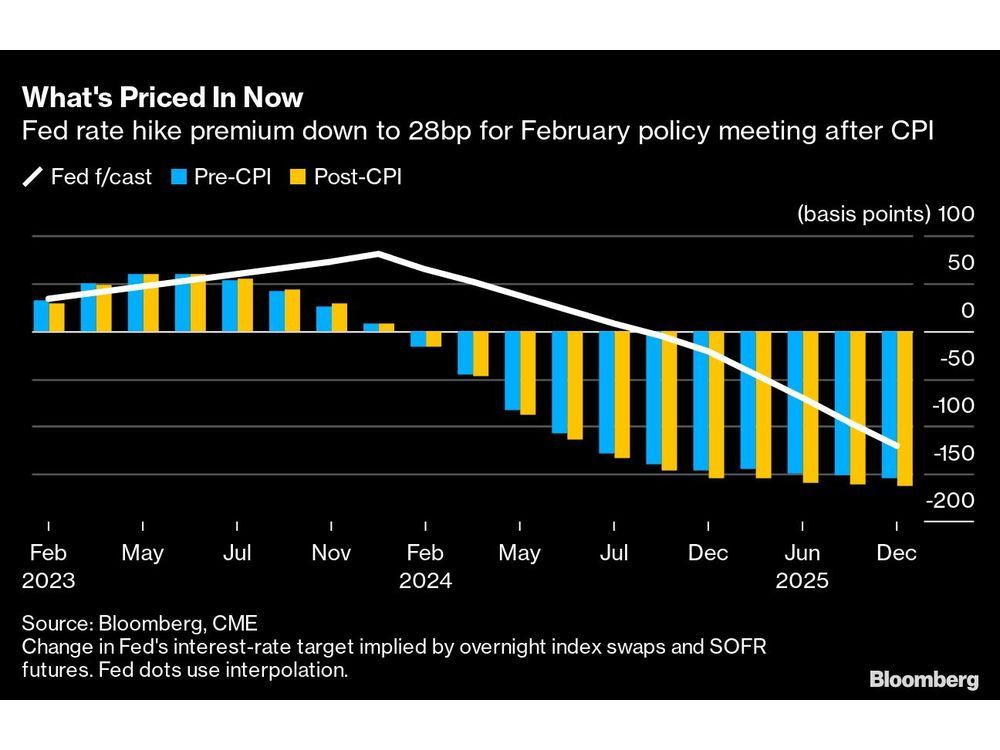

The US Treasury market reached an inflection point Thursday when a report showed that consumer inflation rates declined to the lowest levels in more than a year, and Philadelphia Fed President Patrick Harker 15 minutes later said he favored another downshift in the pace of rate increases. Market-implied expectations for the central bank’s February meeting gravitated further toward a quarter-point hike instead of a half-point, and for the first time gave small odds to the possibility of no move at all in March.

Financial Post Top Stories

Sign up to receive the daily top stories from the Financial Post, a division of Postmedia Network Inc.

By clicking on the sign up button you consent to receive the above newsletter from Postmedia Network Inc. You may unsubscribe any time by clicking on the unsubscribe link at the bottom of our emails or any newsletter. Postmedia Network Inc. | 365 Bloor Street East, Toronto, Ontario, M4W 3L4 | 416-383-2300

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Financial Post Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Short- and intermediate-term yields declined sharply, reaching the lowest levels in three months, while the 10-year slid below 3.5%, extending a rally from about 3.8% at the start of the year. Plenty of uncertainty remains; earlier this week, two other Fed officials predicted an extended stay above 5% for the Fed’s overnight benchmark. But investors are finally looking past the threat of higher policy rates as they set positions.

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

“The market has discounted all the Fed’s language about pushing the terminal rate higher than 5%,” said Ed Al-Hussainy, a rates strategist at Columbia Threadneedle Investments. Having favored long-dated bonds in recent months, he anticipates intermediate sectors will fare best on the approach to the end of the hiking cycle. Eventually, “once the Fed tells us this is the last hike — and March is a decent bet around that — then the front end is there for the taking.”

Bond investors were decimated last year by rising yields as the Fed raised its target range for overnight interest rates by more than four percentage points in response to quickening inflation.

Accumulating evidence that inflation has peaked allowed the Fed to ease up on the brakes in December with a half-point increase following four straight three-quarter-point moves. The latest slowdown in the growth rate of consumer prices in December — excluding food and energy, the fourth-quarter rate was 3.14%, a 15-month low — unleashed a wave of trading.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

In swap contracts referencing Fed meeting dates, the expected peak for the overnight rate declined toward 4.9%. Just 29 basis points of increase are priced in for the Feb. 1 decision — indicating a quarter-point is favored over a half-point — and fewer than 50 basis points are priced in by March.

A blizzard of wagers in short-term interest-rate options after the inflation data anticipated the imminent end of Fed rate hikes and additional declines in market volatility. They included a large one expressing the view that the cycle will pause after February.

“The path of short-term rates is tied to inflation, with a swing factor around that due to how strong or weak the economy is looking,” said Jason Pride, chief investment officer of Private Wealth at Glenmede. “A 5% funds rate is necessary if inflation is running at 6% and 7%, not so when inflation is back down to 3%, and you could see year-over-year headline inflation around 3% by the middle of the year.”

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

Beyond the short-term rate market, the new framework spurred wagers on additional Treasury market gains.

In Treasury futures, Thursday’s rally resulted in big increases in open interest — the numbers of contracts in which there are positions — particularly for 10- and 5-year note contracts. The increase was equivalent to the purchase of $23 billion of the most recently issued 10-year note, about 20% of the amount outstanding.

The 10-year Treasury yield, which peaked last year near 4.34%, has scope to retreat to around 2.5% within six months if the inflation trend is sustained, Al-Hussainy said.

“Most of the risk premium in the long end of the curve reflects inflation and if it comes down faster, or even at the current pace, there’s a big runway for the long end to reprice,” he said.

Advertisement 6

This advertisement has not loaded yet, but your article continues below.

Article content

It may be too soon. A period of consolidation may be in store for the Treasury market after its steep gains.

“The inflation story is not over yet, and there is some market complacency that they have the right Fed playbook,” said Lindsay Rosner, multisector portfolio manager at PGIM Fixed Income.

Treasury yields were led higher last year by short maturities like the two-year, which remains the highest-yielding part of the market at around 4.21%. PGIM expects a reversal of that trend, but it may take some time to get going.

“The steepener is the right trade for this year, and it really starts once the Fed ends hiking,” she said.

What to Watch

Economic calendar:

Jan. 17: Empire manufacturing

Jan. 18: Retail sales; producer price index; industrial production; business inventories; NAHB housing market index; mortgage applications; Fed Beige Book; Treasury International Capital Flows

Jan. 19: Housing starts; Philadelphia Fed Business Outlook; jobless claims

Jan. 20: Existing home sales

Fed calendar:

Jan. 17: New York Fed President John Williams

Jan. 18: Atlanta Fed President Raphael Bostic; Philadelphia Fed President Patrick Harker; Dallas Fed President Lorie Logan

Jan. 19: Boston Fed President Susan Collins; Vice Chair Lael Brainard; Williams

24World Media does not take any responsibility of the information you see on this page. The content this page contains is from independent third-party content provider. If you have any concerns regarding the content, please free to write us here: contact@24worldmedia.com

![txbymt3qyoz[qkgfgf4]a00d_media_dl_1.png](https://smartcdn.gprod.postmedia.digital/financialpost/wp-content/uploads/2023/01/whats-priced-in-now-fed-rate-hike-premium-down-to-28bp-for-.jpg?quality=90&strip=all&w=1128&h=846&type=webp)