Article content

The Office of the Superintendent of Financial Institutions raised the capital buffer financial institutions must hold to three per cent, citing increased risked from high household indebtedness and the rapid rise in interest rates.

Rapidly rising rate environment, geopolitical uncertainty also key risks, OSFI says

The Office of the Superintendent of Financial Institutions raised the capital buffer financial institutions must hold to three per cent, citing increased risked from high household indebtedness and the rapid rise in interest rates.

The financial watchdog also increased the capital buffer’s range, or the policy tool to keep the country’s financial stability in check, to between zero and four per cent starting February 2023, rising from the previous range of zero to 2.5 per cent.

“This new level reflects our observations and high levels of systemic vulnerabilities have persisted and, in some cases, increased in recent quarters,” said OSFI assistant superintendent Angie Radiskovic during a Dec. 8 press conference. “Canadian household debt levels relative to income are approaching record highs, exacerbated by sharply rising debt servicing costs as interest rates have increased. While house prices have begun to decline, they remain elevated after factoring in higher mortgage rates.”

Radiskovic added that highly indebted corporations are more vulnerable to economic shocks in a rising rate environment and sovereign debt levels are elevated worldwide compared to pre-pandemic levels.

“Finally, geopolitical uncertainty remains high, increasing the chance of a global slowdown that spills over into Canada,” Radiskovic said.

Also factored into OSFI’s decision is stress testing various scenarios and taking into account the high-profile acquisitions some of Canada’s Big Six banks have made this year. Radiskovic said banks are required to address all operations and cover all of the risks they’re exposed to, which would include forward-looking statements and contingency plans in their capital planning strategy.

Since the buffer was created in 2018, it has been OSFI’s tool to provide a capital reserve range that applies to Canada’s largest banks. During economic boom times, the reserve is built upon. When the economy hits a period that strains financial institutions, it can be drawn upon to provide support. The buffer comes on top of normal capital ratio requirements that force the banks to keep capital in reserve.

The buffer is baked into the common equity tier 1 ratio (or the CET 1 ratio) that compares a bank’s capital against its risk-weighted assets to measure its resilience in a market downturn.

National Bank of Canada analyst Gabriel Dechaine said OSFI’s move would bring the regulatory minimum CET 1 ratio up from the current rate of 10.5 per cent to 11 per cent as of February, or up to a maximum of 12 per cent given that the capital buffer range now extends to four per cent.

Dechaine added that while the banks would see gradual upward pressure on their capital ratios, National Bank estimates that all the banks aside from the Bank of Montreal have a capital buffer resting well above the regulatory minimum.

“BMO’s capital position suddenly looks a lot weaker,” Dechaine wrote in a Dec. 8 note following the news, referencing BMO’s pending

US$16.3 billion Bank of the West deal.

BMO expects the deal will close within the first quarter next year, though Dechaine expects it could take a bit longer and fall into the second quarter. Should the deal close within BMO’s timeline, Dechaine said the bank’s pro forma CET 1 ratio for that quarter would dip to 10.5 per cent, which is below the new regulatory minimum.

“We note that every 10 (basis points) shortfall represents $365 million of capital,” Dechaine wrote. “The market could assume a larger shortfall, if factoring in typical buffers banks maintain above regulatory minimums.”

The analyst said the bank might have alternatives to raising capital, including the possibility of an arrangement with OSFI to reach the new threshold gradually.

Canaccord Genuity analyst Scott Chan said in a Dec. 8 note to clients that National Bank has the strongest capital position with a CET 1 ratio at 12.7 per cent. Given this position, Chan expects National Bank would be able to deliver higher-than-average dividend increases.

The Bank of Canada engaged in an aggressive rate-hiking campaign over the year that brought the policy rate up 400 basis points to 4.25 per cent, prompting economists to project an economic slowdown heading into 2023.

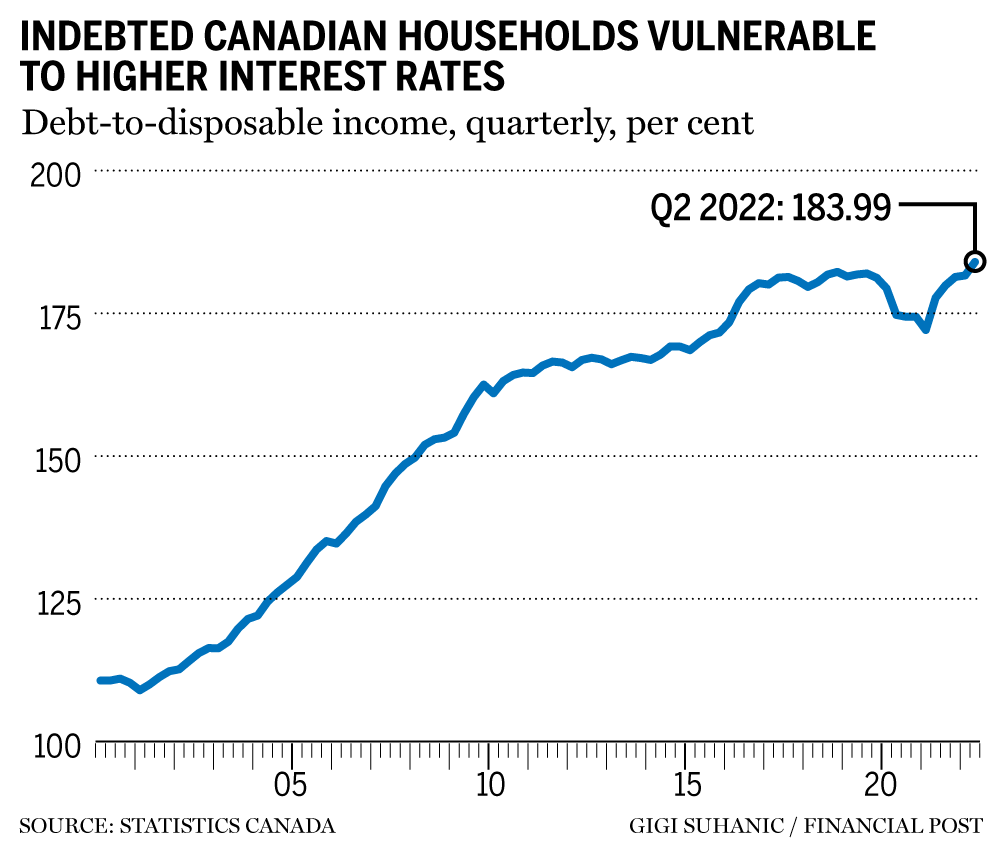

High household debt was an issue OSFI flagged this time last year when it maintained the capital buffer for banks at 2.5 per cent. Since then, the debt-to-income ratio moved from 177.2 per cent in the third quarter of 2021 to 181.7 per cent in this year’s second quarter.

OSFI said it would continue to monitor financial system vulnerabilities and broader economic environment, and was ready to respond through policy to minimize the impacts should these risks worsen.

• Email: shughes@postmedia.com | Twitter: StephHughes95

24World Media does not take any responsibility of the information you see on this page. The content this page contains is from independent third-party content provider. If you have any concerns regarding the content, please free to write us here: contact@24worldmedia.com

A Brief Look at the History of Telematics and Vehicles

Tips for Helping Your Students Learn More Efficiently

How To Diagnose Common Diesel Engine Problems Like a Pro

4 Common Myths About Wildland Firefighting Debunked

Is It Possible To Modernize Off-Grid Living?

4 Advantages of Owning Your Own Dump Truck

5 Characteristics of Truth and Consequences in NM

How To Make Your Wedding More Accessible

Ensure Large-Format Printing Success With These Tips

4 Reasons To Consider an Artificial Lawn

The Importance of Industrial Bearings in Manufacturing

5 Tips for Getting Your First Product Out the Door